How mutual funds work

Important information - the value of investments can go down as well as up so you may get back less than you invest. This information is not a personal recommendation for any particular investment. If you are unsure about the suitability of an investment you should speak to one of Fidelity’s advisers or an authorised financial adviser of your choice.

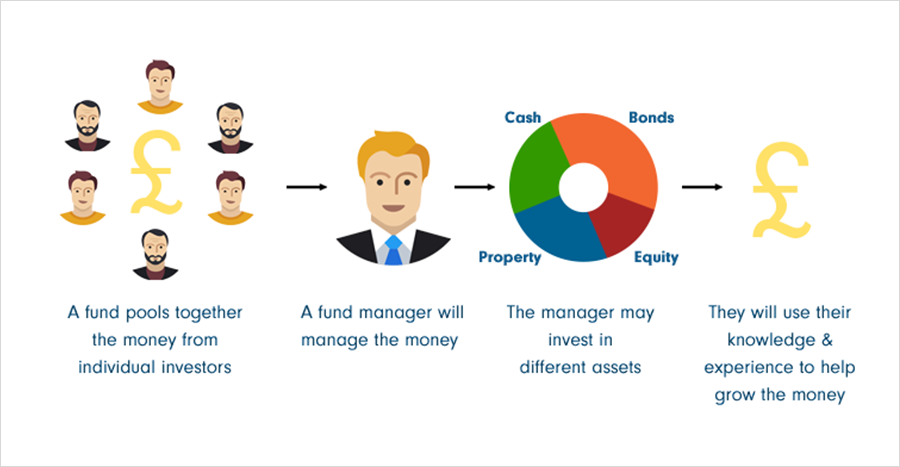

What is a fund?

Funds allow investors to pool their money together, which a fund manager will then invest on their behalf. The manager is responsible for choosing investments for the fund and tries to grow investors’ money by spreading it over a range of company shares, bonds etc., although the growth isn't guaranteed.

Unit trusts, offshore funds and open-ended investment companies (OEICs) can all be referred to generically as funds.

Why invest in a fund?

More investment opportunities

Pool your money with other investors to take advantage of investment opportunities more easily than if you bought the individual assets yourself.

Managed by experts

Active fund managers use their knowledge, experience and research to help your money grow and provide you with an income, if required.

Spreading the risk

Invested across a number of different companies, you’re not relying too heavily on the fortunes of any one company.

Risks of investing in funds

However, there are a few things to consider, as well.

Fund types

These funds are open-ended funds, meaning they can get larger or smaller depending on the number of investors who wish to buy into them.

As more people invest in the fund, the number of underlying shares grows; as they sell, the number reduces.

While offshore funds are exempt from tax, meaning any gains can be reinvested back into the fund without being taxed, how much tax you pay depends on your circumstances, such as the country you live in at the time.

There are two types of property funds: ‘Bricks and mortar’ property funds, and property company funds, such as Real Estate Investment Trusts (REITs).

‘Bricks and mortar’ property funds invest in the buildings themselves. The fund takes responsibility for finding properties, handling the deals, seeking tenants and maintaining the buildings. You get a share of the rents paid by the property tenant, plus returns if the value of the properties owned by the fund increases.

While most property funds generally hold a cash buffer to meet short-term withdrawals, it may be difficult to redeem your investments at times of market stress. This is because the fund manager must sell physical property to meet redemptions, which may take time.

Property company funds invest in the shares of property companies. Global property funds can hold shares in Real Estate Investment Trusts (REITs), which are listed on the stock market and their fund price reflects the value of the properties they own.

Exchange traded funds are similar to the funds mentioned above except that they act like a share themselves, and are openly traded on a stock exchange such as the FTSE All Share. Most ETFs aim to perform in line with a specific index or commodity (like gold) and often have low management fees. Find out more about ETFs.

These are funds registered as public limited companies (PLCs) with their own management teams and boards of directors. They can invest in public and private companies, have a specific number of shares in issue and are traded on a stock exchange themselves. Find out more about investment trusts.

Fund management

Passively managed funds attempt to match or track the movement of a stock market index.

Your investment reflects proportionately the companies listed in a particular index, like the FTSE 100, and the stock market dictates how well your investment does.

Actively-managed funds invest in a collection of companies the fund manager feels can outperform the index. To identify these funds, they analyse company fundamentals, meet the management and work to maintain a balance of good companies that aims to perform better than the market average in various market conditions, but this is not guaranteed.

These funds don’t track the movement of a particular stock market index.

A fund of funds invests primarily in other investment funds rather than directly into individual companies.

They provide an alternative to putting together your own portfolio of funds, monitoring and making changes. They provide ready-made portfolios managed by expert fund managers.

Evaluating funds

It takes time, experience, knowledge and skill to work out which fund could be the one right for you. Here’s what you need to consider along with your personal circumstances (like how much risk you’re willing to take).

- Age of the fund - Do you want a fund with an established track record, or get in early with a new fund launch?

- Size of fund - This indicates the fund’s popularity and past success at attracting investors. However, some funds can be so large it’s difficult for the fund manager to run it. A small fund is sometimes easier to manage.

- Fund manager tenure - Consistent fund performance often relies on a fund manager having managed it for some time. But watch out - star performers can change jobs.

- Independent ratings - Companies such as Morningstar, Standard & Poor’s and Moody’s provide independent ratings for funds’ performance, creditworthiness and consistency of management.

- Charges - Look closely at all the fund charges - are the ongoing charges excessive, are there penalties for withdrawing your money?

Differences between funds and other investments

Related articles

Top 10 best-selling Junior ISA funds of 2026

Ideas to help fund your child’s future

Jemma Slingo

Fidelity International

23 July 2026

4 growth funds for your ISA

Tax efficient growth ideas from the Select 50

Nick Sudbury

Investment writer

20 July 2026

What is a money market fund? The basics

Understanding the role of cash funds in a portfolio

Becks Nunn

Fidelity International

20 July 2026